Portfolio Studio

Portfolio Studio is the workspace for a single saved portfolio. Where the Portfolios Hub is about building portfolios, the Studio is about understanding and preparing one: what it does, how its capital should be split, and whether it can survive the real world.

Where to find it: In the app sidebar, open Portfolio Studio — it opens your most recent portfolio (or pick one from the Library). The Studio has three main tabs:

| Tab | Question it answers |

|---|---|

| Analyze | What does this portfolio actually do? |

| Allocate | How should capital be split across its strategies? |

| Robustness | Can it survive stress, and how much capital does it need? |

Every portfolio also earns a portfolio-level CSI — the same 0–100 scale as individual strategies, so you can directly compare a portfolio to the strategies inside it.

Analyze Tab

The default landing tab. It reads top-to-bottom like a briefing:

Decision Summary

A row of chips at the top gives the headline verdict — key stats and any warnings that deserve attention. An Edit Portfolio button lets you adjust the composition without leaving the page.

Combined Equity Curve

The portfolio's merged equity curve with a $ / % toggle and brush zoom for inspecting specific periods. This is the curve that matters — individual strategy curves can look ragged while the combination is smooth (that's diversification working).

Contracts Open Over Time

A stacked bar chart of how many contracts each strategy holds through time. Reveals concentration moments — periods when many strategies are positioned at once and your margin and risk usage spikes.

Drawdown Analysis

Portfolio-level drawdown depth and duration, following the same $/% mode as the equity chart. Compare it against the worst member strategy's drawdown to see how much diversification is saving you.

Strategy Allocation

How capital and risk are distributed across members — switchable between a contribution heatmap, bars, table, and treemap view.

Period Performance & Calendar Returns

Performance sliced by period, plus a month-by-year heatmap — the portfolio version of the same views in the Quality Report.

Strategy Breakdown

Detailed per-strategy metrics inside the portfolio context: who's contributing profit, who's contributing risk, and who's dead weight.

Risk Decomposition

Splits portfolio risk by source. A portfolio where one strategy contributes 70% of the risk isn't really diversified, no matter how many names are in it.

An insights footer links you to the logical next steps in Allocate and Robustness.

Allocate Tab

Compares capital-split methods and sizes your portfolio in whole contracts. It's a big enough topic to have its own page — see Allocation Methods for every method and setting explained.

In short: you set your capital, pick methods from three tiers (Foundation, Professional, Institutional), click Run Comparison, and evaluate the results on a Risk / Return Map, an Equity & Drawdown overlay, and a Comparison Table. Save the winner as your portfolio's allocation.

Robustness Tab

One configuration panel, one Run Robustness Check button, one integrated answer. This replaced the older separate backtest tools (walk-forward, Monte Carlo, and stress testing now run together as a single check).

Configuration

| Group | Settings |

|---|---|

| Risk Targets | Target Risk of Ruin, Target Max Drawdown, Target Annual Volatility, Ruin Threshold, and Confidence Level (P90 / P95 / P98 / P99) |

| Monte Carlo Resampling | Simulations count and Block Size in days (blocks preserve streaks — see Block Bootstrap) |

| Walk-Forward | IS Window and OOS Window in months — how history is split into "training" and "verification" segments |

| Transaction Costs | Toggle on to model Fixed ($ per trade), Variable (bps), and Slippage (bps) |

| Size Capital On | Full History or Out-of-Sample — whether capital requirements are computed from everything or only the verification window (OOS is the conservative choice) |

Results — the five pillars

- Robustness Verdict — the headline: does this portfolio hold up? Includes "How Much Money Does It Take?" at a glance.

- Capital Sizing — required capital to meet your risk targets, the binding constraint (which target is the limiting factor), and the Out-of-Sample Haircut — how much more capital the conservative OOS view demands. A goal-seek panel lets you adjust targets and re-solve.

- Outcome Distribution — the spread of simulated outcomes: percentile bands for profit and drawdown across all Monte Carlo runs.

- Crisis Scenarios — how the portfolio would have navigated historical crisis windows.

- Out-of-Sample Validation — walk-forward results including the out-of-sample equity curve. If the portfolio only performs in-sample, it's curve-fit — see Why Strategies Fail.

Saved Robustness Runs keeps prior runs so you can reload and compare configurations without re-simulating.

Tip

Run Robustness with Size Capital On: Out-of-Sample before trading a portfolio live. The OOS haircut is the single most honest number in the app — it tells you what the portfolio needs when history doesn't repeat politely.

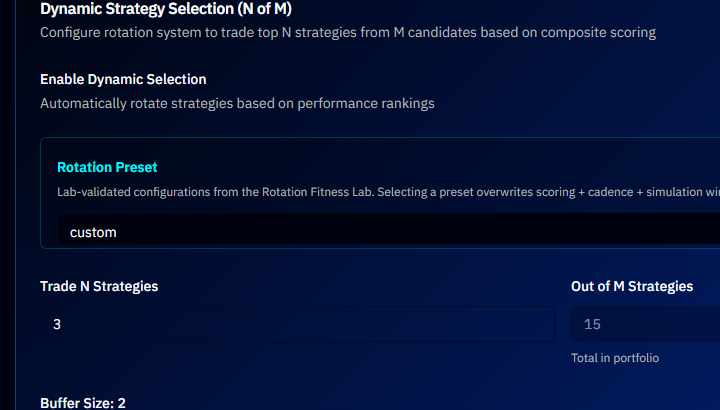

Rotation (Limited Preview)

An advanced capability currently in limited preview: instead of trading all member strategies at once, Dynamic Strategy Selection (N of M) keeps a bench of M validated strategies and actively trades only the top N, re-ranked on a schedule (e.g. monthly on the last trading day). Configuration includes the selection metric (composite risk-adjusted rankings, CSI, or Health-based), a buffer to reduce churn, and a backtester to validate the rotation rules before enabling them. A Rotation History view logs every rebalancing event.

If you don't see these tabs, they aren't enabled for your account yet.

Common Questions

Analyze, Allocate, Robustness — in what order? That order. Understand what you own (Analyze), decide how to size it (Allocate), then verify it survives (Robustness).

Do the tabs affect my saved portfolio? Analyze is read-only. Allocate changes your portfolio only when you explicitly save a candidate. Robustness never modifies the portfolio — it saves separate run results.

Why does my portfolio's CSI differ from its strategies' scores? The portfolio is scored on its combined equity curve. Diversification can lift the portfolio's Risk profile far above any member's — or correlation can drag it below.

Tip

Ready to see this in action? Start your free trial — no credit card required.